The Tax Reform for Acceleration and Inclusion (TRAIN) or Republic Act 10963 is now in full swing. With all industries lining up with its implementation, the real estate industry is also following through. Here are some of the things that were affected by the TRAIN Law.

Documentary Stamp Tax

The documentary stamp tax (DST) has been doubled from 1.5% to 3%.

Estate Tax

Estate tax is now set at a flat rate of 6% on the amount in excess of P5 million.

Below are exempted from estate tax:

- Estates with net value of P5 million and below

- Family homes that are valued at P10 million or less

Donors Tax

Same with estate tax, donors tax has now been set to a flat rate of 6% regardless of relationship between the donor and donee. Previously, it was 2% to 15% for related donor and donee and 30% for strangers.

Gifts that are below P250,000 are exempted from this tax. The new rate of 6% are applied for donations of P250,000 and higher.

Value Added Tax

Value Added Tax (VAT) is the tax levied on the sale, barter, exchange or lease of goods, properties or services. This is currently at 12% rate. This is a form of tax which can be passed on to the buyer or consumer.

VAT for the sale of goods and services was levied when one reaches P1,919,500.00 and all VAT registered individuals and businesses. Importation of goods is also vat-able. With the TRAIN Law in full swing, the new threshold is P3,000,000.00. So how does it affect Real Estate in particular.

VAT for the sale and lease of Properties

Previously, the sale of lot only was at 1,999,500 while house and lots are at 3,199,200. No news as to whether this has been updated.

Condominium association dues are exempted from paying VAT. Rentals and leases below P15,000 per month are also VAT exempted.

Socialized housing, or houses priced at P450,000 and below, low-cost housing or any property for sale, with prices of P3 million and below are VAT exempted from 2018 to 2020 only.

VAT for Individuals and companies

P3 Million or below annual gross sales or income

This is applicable for Self-employed and professionals with annual gross sales or income receipts of P3 Million and below have the option to choose with these two tax rates:

- Eight percent (8%) of gross sales or receipts and other income, in excess of P250,000; No need to use the income tax table and pay the 3% percentage tax;

- Graduated income tax rates of 0% to 35% based on the net taxable income, plus 3% percentage tax

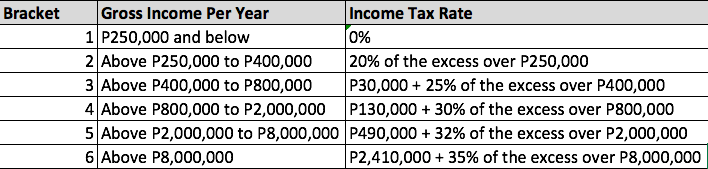

BIR Income Tax Table (2018-2022)

BIR Income Tax Table (2023 onwards)

8% Withholding Tax for Self-employed and Professionals

The two-tier rate of 10%; for income that are less than P720,000 every year or 15%; for income more than P720,000 per year was replaced with this 8% Withholding Tax until a professional or self employed individual reaches the VAT threshold of P3,000,000.

This is applied regardless of the amount as reiterated in BIR’s Revenue Memorandum Circular No. 1-2018 issued on January 4, 2018 which states that:

“Change in the Creditable Withholding Tax Rate on lncome Payments to Self-employed lndividuals or Professionals

The following lncome Payments to Self-employed lndividuals or Professionals shall be subject to Eight Percent (8%):

1. Professional fees, talent fees, commissions, etc. for services rendered by individuals;

2. lncome distribution to beneficiaries of Estates and Trusts;

3. lncome Payment to certain brokers and agents;

4. lncome Payments to partners of general professional partnership;

5. Professional fees paid to medical practitioners; and

6. Commission of independent and/or exclusive sales representatives, and marketing agents of companies.”

Annual gross sales or income of above P3 Million

A simpler tax rate is to be followed for those earning above the VAT threshold of P3,000,000. If the gross income or sales receipts total is more than P3 million, the Income tax table is to be followed on the net taxable income, plus VAT.

Comments

-

December 22, 2018 at 12:45 pm

Dennis chua sevilla

-

June 16, 2019 at 2:13 pm

buyingph

-

February 26, 2020 at 8:29 am

buyingph

-

February 26, 2020 at 8:30 am

buyingph

-

-

-

July 9, 2019 at 11:54 pm

Jay-r

-

July 11, 2019 at 12:34 am

buyingph

-

-

January 29, 2020 at 12:52 am

SEO Referral Program

-

January 29, 2020 at 10:39 am

Ritz

-

May 22, 2020 at 8:26 am

buyingph

-

-

February 11, 2020 at 5:18 pm

Kaye

-

February 26, 2020 at 8:31 am

buyingph

-

-

February 16, 2020 at 12:48 am

AffiliateLabz

-

March 30, 2020 at 11:22 pm

Mr R Naylor

-

May 22, 2020 at 8:29 am

buyingph

-

-

May 19, 2020 at 5:52 pm

salesagent

-

May 22, 2020 at 9:01 am

buyingph

-

-

March 9, 2021 at 3:57 am

flo